The awkward thing about smart home AI in 2026 is that the devices are getting better faster than the home is getting coherent. A premium oven can recognize food. A refrigerator can recommend what to cook. A thermostat can learn occupancy patterns. A camera can classify motion. None of that automatically means the house understands what is happening across the kitchen, hallway, garage, panel, and living room.

CES 2026 made the gap unusually visible. GearBrain’s show-floor reporting pointed to a simple incompatibility that says more than another stage demo: LG’s AI vision oven does not talk to Samsung’s SmartThings fridge, even though both sit in the same real kitchen scenario. Alexa+ and Gemini were also framed as improving their own ecosystems rather than coordinating across them.[1] That is the part that matters after the keynote. The oven may be smarter. The fridge may be smarter. The dinner routine is still stuck at the brand boundary.

That is why the useful question is not whether AI belongs in the home. It already does. The question is whether AI lives inside each manufacturer’s app, or whether some neutral layer can see enough of the home to make useful decisions across brands.

Smarter Devices Are Creating Dumber Boundaries

A mixed smart home is rarely a clean architecture diagram. It is usually a slow accumulation: a few smart bulbs from one sale, a thermostat from an HVAC installer, a doorbell camera from a security bundle, a Sonos speaker that outlived two hubs, a Lutron dimmer because it just works, and maybe an appliance app that appeared after a kitchen remodel.

GearBrain’s AI agent company guide puts the average U.S. connected home at 15 to 20 devices across more than five brands, with 57% of households owning at least one smart device.[2] Those are averages, not a law of nature; some homes are much simpler and some are far messier. But the shape is familiar. The home is already multi-brand before AI arrives, and AI is now being added mostly inside the same brand lanes that caused the original fragmentation.

That produces a strange upgrade path. The appliance becomes more aware of food, but not of the household’s energy constraints unless its own ecosystem exposes them. The speaker becomes better at answering questions, but may not actuate the lighting, shades, security mode, and media system with the same reliability across platforms. The energy app can optimize what it sees, while the rest of the load profile remains somebody else’s problem.

The user experiences this less as a standards debate than as small operational drag. One routine works only from one app. Another loses an advanced option when moved into a platform. A firmware update changes a device capability. A cloud service outage turns a voice command into a shrug. The house is full of intelligence, but the intelligence does not share enough context.

Matter Helps Pairing. It Does Not Give the Home a Brain.

Matter deserves credit before it gets blamed for things it was not designed to do. By 2026, there are more than 750 Matter-certified products, and cross-platform pairing has become genuinely more practical than the old ritual of guessing which hub, bridge, or assistant a device would tolerate.[3] For anyone starting from scratch, that is enough progress to change buying advice; it is why a Matter-first approach still belongs in a modern setup guide like Build Your First Matter Smart Home in 2026.

The limitation is that pairing is not coordination. Matter can make it easier for a bulb, plug, sensor, lock, or thermostat to show up in multiple ecosystems. It does not create a shared AI model of the home’s routines, appliance states, energy priorities, security context, or room-level intent. Hands-on testing summarized by ClarityTechHub found that advanced features such as AI routines and multi-device scenes often remain ecosystem-specific, and buyers still need manufacturer apps for deeper configuration.[4]

| Layer | What It Improves | What It Usually Does Not Solve |

|---|---|---|

| Matter pairing | Getting supported devices onto multiple platforms with less friction | Shared AI reasoning across brands |

| Manufacturer apps | Deep control of that brand’s features | Neutral coordination with rival ecosystems |

| Voice assistants | Natural commands and broad consumer access | Reliable local orchestration when cloud APIs or ecosystem permissions get in the way |

| Neutral orchestration | Cross-brand visibility, rules, context, and local control | Polished mass-market simplicity by default |

This distinction matters because a home can be Matter-compatible and still poorly coordinated. The device joins the network. The basic switch works. Then the interesting part begins: can the kitchen occupancy sensor, the panel load data, the thermostat schedule, the music state, the door lock, and the appliance mode participate in one decision without handing the whole house to a single vendor?

Why Big Tech Keeps Stopping Short

Amazon, Google, Apple, and Samsung can make smart home control easier. They also have reasons not to become a truly neutral intelligence layer. A platform that gives equal depth to every rival’s devices weakens the gravity of its own ecosystem. The commercial incentive is to make cross-platform support good enough to reduce buyer hesitation, while reserving the best experience for devices, services, subscriptions, and assistants inside the platform’s preferred orbit.

That does not make the big platforms useless. For many households, a polished app and a familiar voice assistant are the difference between a smart home that gets used and a box of abandoned sensors. Convenience counts. But convenience becomes expensive when every advanced feature quietly asks the homeowner to choose a camp. That is the trap covered in The Smart Home Ecosystem Trap: Which Platform to Buy Into in 2026: the more comfortable the app feels, the easier it is to miss where the walls are being built.

Cloud-based AI assistants add another boundary. They can be excellent at interpreting language, generating routines, or bridging services, but they are only as capable as the APIs, permissions, latency, and internet connection underneath them. A setup like How to Set Up ChatGPT to Control Your Smart Home can be useful, especially for experimentation, but it does not erase the need for a dependable local control plane when lights, locks, HVAC, and energy loads need to behave even when the cloud is slow or unavailable.

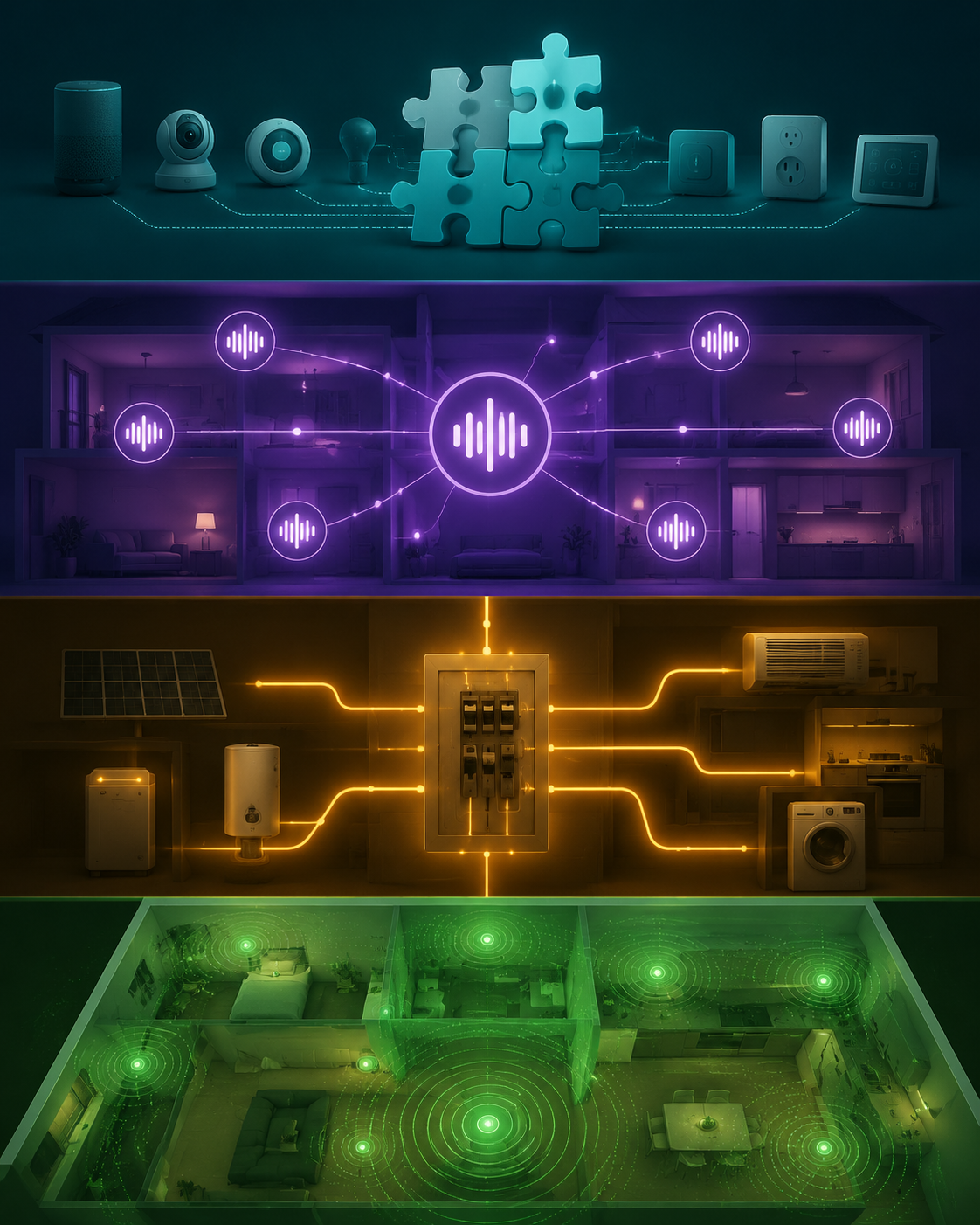

The Neutral Layer Is Where the Interesting Startups Are

The most credible AI smart home startups and projects in 2026 are not all doing the same job. Some sit at the protocol and integration layer. Some interpret voice and intent locally. Some move intelligence into electrical infrastructure. Some sense presence without cameras. Their common advantage is that they have less to protect at the hardware-ecosystem level. They can afford to ask a more useful question: what does the house need to coordinate, regardless of whose logo is on the device?

Home Assistant: Open Software Scale Beats Perfect Vendor Permission

Home Assistant’s advantage is not glamour. It is coverage. GearBrain’s guide cites more than 2,000 integrations, plus support for local vision processing through a Coral AI accelerator and the launch of its Matter server.[2] That breadth changes the character of automation. Instead of waiting for a manufacturer to decide which partners deserve advanced access, the home can often pull devices, sensors, and services into one local model through community-built integrations.

That matters most in the unglamorous edge cases. A motion sensor from one brand can help decide whether a different brand’s thermostat should hold temperature. A leak sensor can trigger lights, notifications, and a shutoff valve without needing all three to belong to the same app family. A local camera or vision sensor can contribute occupancy context without making every automation dependent on a remote AI service.

Home Assistant is not the easiest path for every buyer. It still asks more of the person installing and maintaining it than a single-brand app does. Integrations can break, terminology can be dense, and powerful local control has a way of becoming a weekend project. But as a neutral orchestration layer, it solves a real problem that glossy ecosystems often route around: it tries to make the whole mixed-brand home visible.

Homey Pro: The Hub as a Protocol Translator

Homey Pro sits in a related but more packaged category: the multi-protocol hub. Its pitch is not that every device becomes magically intelligent. It is that the home needs a practical translation layer across radios, platforms, and automations before higher-level intelligence has enough inputs to work with. That is less exciting than an AI appliance demo, but it is closer to the day-to-day problem in homes built over several years.

The tradeoff is familiar. A packaged hub can be more approachable than a full DIY stack, but it may not match the long-tail integration depth or community velocity of Home Assistant. Its importance here is as a category marker: neutral intelligence needs plumbing before it needs personality.

Josh.ai: Local Voice Control for Homes That Are Already Complicated

Josh.ai earns attention for a different reason. It operates in high-end installed homes where the system is already expected to coordinate Crestron, Lutron, Sonos, Control4, shades, lighting, audio, climate, and scenes without treating the homeowner as a beta tester. Its own 2025 wrapped report said it processed 158 million actions in 2025, up from 83 million in 2024, including 5 million voice commands.[5] ResTechToday also described Josh.ai’s local, on-device approach and its work across major luxury-control ecosystems without cloud dependency.[6]

Those usage numbers are company-reported, so they should not be read as independent proof of market dominance. They are still useful because they describe a heavy operational workload in exactly the kind of environment where brittle automation gets exposed quickly. A luxury integrator cannot survive long on a demo that only works when the internet is perfect and every subsystem belongs to the same brand.

The more interesting part is the architecture. A local voice and knowledge-graph layer can understand that “turn off the kitchen” may involve lights, music, shades, display panels, and maybe a scene state, depending on the room and the installed hardware. The goal is not merely speech recognition. It is mapping intent to devices across a messy installed base, then executing without sending the whole home’s control path through a cloud dependency.

That does not make Josh.ai a universal answer. It is aimed at professionally installed, higher-cost systems, not the average apartment with three bulbs and a smart speaker. But it shows one route to serious smart home AI: build the intelligence layer where coordination, local reliability, and cross-brand execution are not optional features.

SPAN: Energy Intelligence Belongs Near the Panel

SPAN approaches the smart home from a less decorative place: the electrical panel. That is a good sign. Energy coordination is hard to fake with an app dashboard because the home’s real constraints are physical loads, circuits, batteries, solar, EV charging, backup power, and utility conditions. Latitude Media reported that SPAN had reached unicorn valuation and was building a brand-agnostic smart electrical panel layer, while also testing an XFRA edge node with Nvidia and PulteGroup to treat homes as distributed AI compute nodes.[7]

The panel is a natural neutral layer because it does not care whether the load came from a Samsung appliance, an LG appliance, an HVAC system, an EV charger, or a battery. If the orchestration problem is partly about seeing across brands, electrical infrastructure has an advantage over a device app: everything eventually becomes load.

The caveat is important. The XFRA Node work described with Nvidia and PulteGroup remains a pilot as of April 2026, not a product that ordinary homeowners can buy and install.[7] A pilot can signal direction, but it does not prove deployment, pricing, maintenance, or long-term interoperability. SPAN’s strongest current argument is the more grounded one: energy AI makes more sense when it starts from a brand-agnostic view of circuits instead of a single manufacturer’s appliance list.

ALLIE: Ambient Sensing Without Turning Every Room Into a Camera Feed

ALLIE by Arqaios broadens the pattern into sensing. GearBrain described ALLIE as using mmWave radar sensors embedded in standard fixtures such as light switches and outlets for brand-agnostic presence and fall detection, with local processing and no cameras.[2] That combination matters because a home cannot coordinate well if it does not know whether rooms are occupied, but cameras are a poor default answer for private spaces.

Presence is one of those inputs that quietly improves everything else. Lighting becomes less dependent on crude motion timers. HVAC can respond to actual room use. Safety routines can distinguish a vacant room from a possible fall event. The useful intelligence is not in making a single sensor clever; it is in allowing that local context to inform other systems without trapping the signal inside one brand’s app.

What Counts as Real Transformation

The startups that matter most are not simply adding chatbots to dashboards. They are moving smart home AI toward layers that can observe, decide, and act across boundaries. That is the difference between a clever device and a coherent home.

- Integration layers make mixed-brand devices visible enough to automate together.

- Local voice and knowledge-graph layers translate human intent into cross-system action.

- Infrastructure layers coordinate energy from the circuit level instead of the app level.

- Ambient sensing layers give the home context without requiring cameras everywhere.

None of these layers has to replace every consumer platform. A normal household may still use Apple Home, Google Home, Alexa, or SmartThings for daily control because the interface is familiar and other people in the house already know how to use it. The neutral layer can sit underneath or beside that experience, doing the less visible work of keeping devices, automations, sensors, and energy rules from collapsing back into brand islands.

The standard should be practical. Can the layer see enough of the home? Can it coordinate across enough brands? Does it keep advanced functions from becoming hostage to one manufacturer’s roadmap? Can important automations keep running when the internet is not the center of the system? Does it avoid solving lock-in by creating a new lock-in?

By that standard, Matter is necessary but not sufficient. Big Tech platforms are useful but conflicted. Manufacturer AI can improve individual devices but often deepens the boundary around them. In Q3 2026, the strongest work is happening where startups and open projects build neutral orchestration: software that integrates, voice systems that act locally, electrical panels that see across brands, and sensors that provide context without demanding a camera in every room.

The caveats stay on the table. Josh.ai’s action volume comes from its own reporting. SPAN’s edge-node work is still a pilot. Matter’s large product count includes many basic devices, not a mature universe of AI-capable products. Company savings claims in the broader energy-AI market can vary sharply by home. The practical judgment is narrower than a victory lap for any one startup: the smart home is not becoming unified just because devices are gaining AI. It becomes more genuinely smart only when intelligence can coordinate across brands without hardening into another closed ecosystem.

References

- CES 2026 Confirms the Future of the Smart Home, GearBrain

- AI agent companies guide, GearBrain

- Matter 2026 status review, Matter-smarthome.de

- Matter hands-on testing, ClarityTechHub

- 2025 wrapped report, Josh.ai

- Josh.ai local coordination report, ResTechToday

- SPAN XFRA edge node report, Latitude Media, April 2026

Updates & Corrections

Protocol specifications and platform features change rapidly — especially with Matter version evolution. Report version changes, certification count updates, or platform policy changes that have occurred since the last editorial review.

Comments

Join the discussion with an anonymous comment.